Carrying on the Domino's Legacy

Wingstop (WING) Coverage Initiation Report

I didn’t even know Wingstop existed until about three years ago, and I still haven’t gotten around to trying it. This did get me thinking, though; what if most people are like me and haven’t even heard of Wingstop? Wouldn’t this create a tailwind for average unit volumes? Based on that first genesis, I began following the company, and I would say I am an expert now.

A Brief History

The founding of Wingstop dates back to 1994, when Antonio Swad opened the first location in Garland, Texas, after a brainstorm in which he decided chicken wings should be more than an appetizer. In 1997, Wingstop launched its franchising model, opening the first franchised locations in 1998. In 2003, the company was acquired by Gemini Investors, and the founder, Antonio Swad, exited to focus on his other restaurant venture, Pizza Patrón. In 2010, Wingstop changed hands, moving under the influence of Roark Capital Group and, in the same year, opening its first international location in Mexico. In 2015, the company completed a successful IPO and listed on the NASDAQ under the ticker WING. Finally, in 2025, Wingstop opened its 3,000th location.

Management

Michael Skipworth is the current CEO of Wingstop. He has previously served in the CFO and COO roles at Wingstop, prior to stepping up as CEO in 2022. He first joined Wingstop in 2014, about a year before it went public. He has focused on improving the menu (adding chicken sandwiches) and digital integration. He has set a long-term goal for Wingstop to have 10,000+ locations and reach $3 million in average unit volumes (AUV).

Capital Allocation

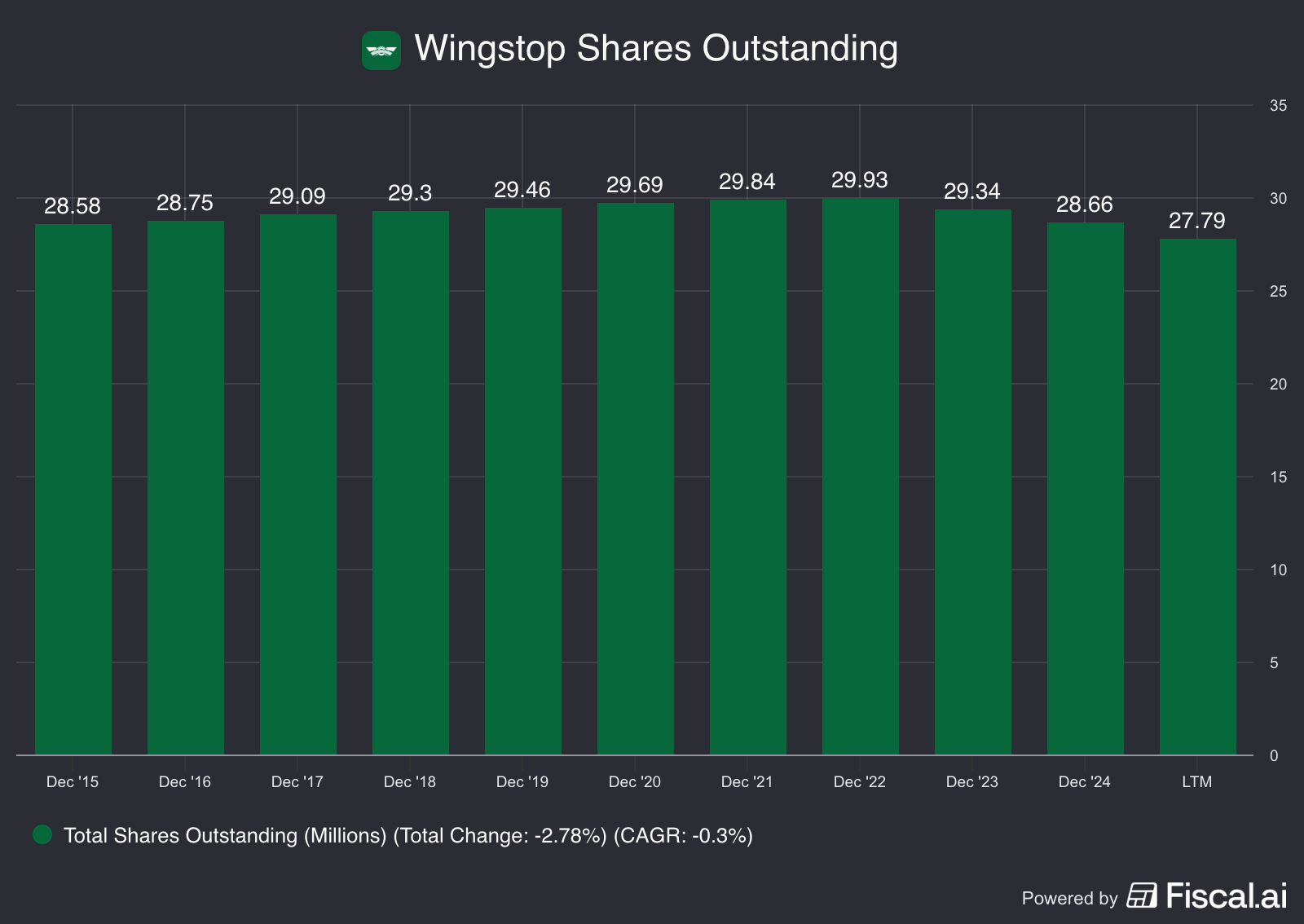

They have recently started aggressively buying back stock, but they also have a dividend. Occasionally and seemingly at random, management will declare a special dividend. This dividend is funded by money borrowed against their brand, which works because of their business model (covered later, and it isn’t a red flag, but look into it if you are worried).

Business Model

Wingstop is a quick-service restaurant that offers classic and boneless chicken wings and chicken tenders, cooked-to-order. Wingstop has over 3,000 locations and is headquartered in Dallas, Texas.

Wingstop’s strategy is to franchise as much as possible. This has resulted in 98% of Wingstop locations being franchised. Wingstop has a strict franchise policy meant for experienced franchisees that will steward the Wingstop brand well and drive growth for Wingstop.

Minimum personal net worth of $1.2 million

Minimum personal liquid cash of $600,000

Minimum commitment to build and manage 3 Wingstop locations

Mandatory experience in operating multi-location restaurants

Absentee ownership is prohibited (operator must live in the same city as the location)

135 hours of required on-the-job experience and 40+ hours of classroom learning in Dallas, Texas.

Franchisees also have to pay Royalty and Ad fees of 6% and 4-5%, respectively, of gross sales every year.

Wingstop’s highly franchised model is the main contributor to Wingstop’s 85% gross margins, almost 26% operating margins, and 27% returns on invested capital (ROIC). All of this means that Wingstop is basically a cash cow, allowing management to return a ton of cash to shareholders. Additionally, the payback period for a Wingstop is targeted to be two years or less, and over 73% of sales are online.

Industry

Wingstop is in a weird spot competition-wise, because, obviously, they compete against every other quick-service restaurant like McDonald’s and Wendy’s, but only one really competes on chicken wings, Buffalo Wild Wings. However, I think these two companies are fundamentally different. Wingstop focuses on take-out sales and quick, quality, efficient service, while Buffalo Wild Wings focuses on creating a fun dine-in experience for people to go and watch sports with their friends.

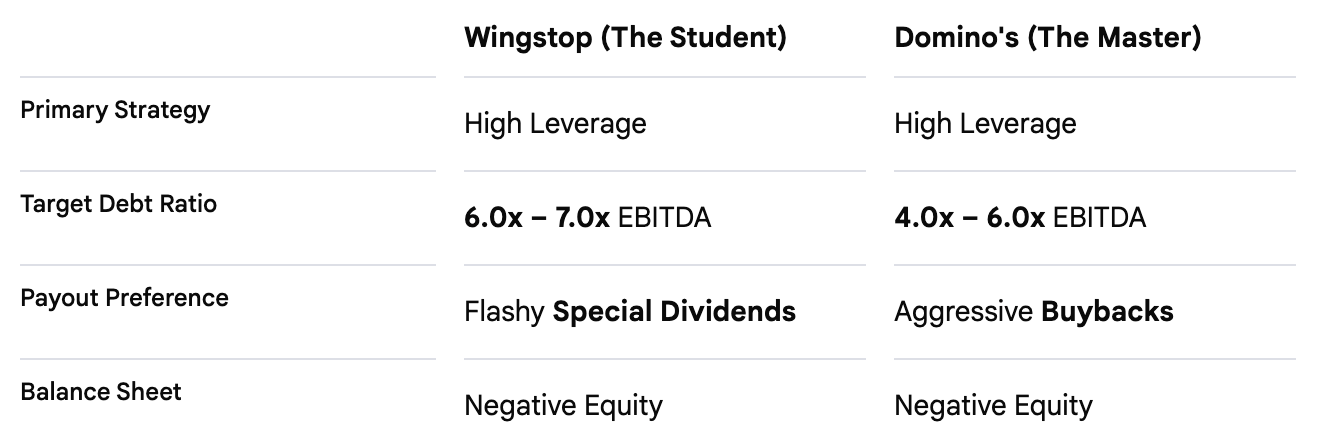

There is one stand-out peer that has a structurally similar business model, Domino’s. Both focus on quality, speed, and take-out and rely on a heavily franchised, asset-light model designed for efficiency and not so much dine-in. Domino’s also does a similar thing, mortgaging its brand to pay dividends and buy back stock, pioneering the method called “Whole Business Securitization,” which I would encourage you to research more because it is a little hard to explain in this research report.

Tailwinds and Growth Drivers

Wingstop has one solid tailwind: not enough people know about their brand. As more people try Wingstop, they will likely stick around. This provides a good runway for average unit volumes to tick up over the years.

Growth in Wingstop’s revenue should primarily come from unit count expansion. Management has set a goal of 10,000 Wingstop locations with no target date, only saying they are looking to achieve this sooner rather than later. They are guiding for 10%+ unit count growth. Importantly, the target implies 6,000 locations in the United States and the other 4,000 internationally. An agreement has been signed for potentially 1,000 locations in India, showing that management is aggressively pursuing this target. There is also the possibility of margin expansion coming from potential pricing power in their fees, which could gradually go up as average unit volumes increase and the relationship with Wingstop proves to be good for franchisees, especially because of their recent push for store efficiency and the launch of Wingstop Smart Kitchen, decreasing time to serve down to 10 minutes, representing a 50% reduction.

Headwinds

There are a few risks I would like to identify in Wingstop. The first one is that comps could be unstable if there is any more deterioration in the consumer, but this should be at least partially offset by international diversification. Additionally, and this is the biggest risk I see, if something happens with Wingstop’s reputation among its franchisees that causes Wingstop to lose its appeal, this could present a headwind to store count growth because they rely heavily on franchising.

The Numbers

Right now, Wingstop trades for 40x trailing EV/EBIT and 17x forward EV/EBIT. If you prefer the price-to-earnings metric, Wingstop trades for 36x trailing P/E and 23x forward P/E. Overall, it isn’t super cheap in absolute terms, but when considering its 25% 10-year revenue compound annual growth rate, it seems justified. Wingstop currently has $237 million in cash and equivalents on its balance sheet, accompanied by $1.2 billion in long-term debt, incurring about $35.7 million in interest expenses every quarter. Wingstop has three tranches of its long-term debt. $473 million is due in 2027, $248 million is due in 2029, and $500 million is due in 2034.

All of this debt is backed by the Wingstop brand, meaning if Wingstop cannot meet its obligations, the company will be operated under a tiered repayment approach. First, cash is diverted from operating activities to a special account. Then, if the business further deteriorates, the dividend is cut and buybacks stop to pay bondholders. If this fails, the management team is fired, and the business is run solely to pay back bondholders by a third-party “Back-up Manager“. If all else fails, the company is sold to someone (private equity, private buyer, or a company) to repay bondholders. This isn’t necessarily a red flag, but certainly something to watch out for.

Moving on to 5-year growth assumptions for the base case, I think 3% average same-store sales growth is doable and 10% unit count growth, meaning 13% revenue growth overall. This would result in $1.25 billion in revenue 5 years out, and assuming operating margins do not change, that means Wingstop will generate about $340 million in operating income in 2031. All of this means Wingstop is trading at about 18.5x EV/5-year-out operating income and, assuming an exit multiple of 25x, Wingstop has the potential for 35% returns over the next five years.

*Disclaimer* You may disagree with my growth assumptions. These assumptions are not guaranteed to happen, and I could be wildly off. Always do your own modeling with your own assumptions. Also, I do not factor in stock-based compensation, but I recommend that you at least think about it when doing your own modeling. Also acknowledge that if these assumptions don’t work out, the investment will likely result in a loss of capital.

The Thesis

The Wingstop thesis rests on successful nationwide expansion, coupled with good capital returns, to provide upside for its investors.

Happy investing, Cade

If you have any suggestions for a future write-up you would want to see, please leave a comment or put it in the subscriber chat.

Please remember that I am not a financial advisor, and anything I say is not formal financial advice. I may buy, sell, or hold securities discussed and may plan to buy, sell, or hold them in the future.

Do you have more info on the smart kitchen concept? I see Chipotle and others using Hyphen to make bowls faster. Can seriously benefit unit economics by shortening lines, improving margin and helping online orders.

Hey Cade! Do you have an idea of what it’s long-term debt is made up of?